Oracle Stock Could Surge by 200% in the Next 5 Years

Oracle(NYSE: ORCL) has been a steady performer on the stock market over the past five years, delivering respectable gains of 230% to investors and outperforming the Nasdaq Composite‘s 143% jump by a handsome margin. But the technology giant has been under pressure this year.

Shares of the company that’s known for providing database management and cloud services have dropped 7% in 2025 as of this writing, roughly in line with the Nasdaq’s move. Oracle’s recently reported results for the third quarter of fiscal 2025 (ended on Feb. 28) didn’t help matters; the stock dropped following the release of its report on March 10, but has since recovered.

The company’s anemic growth wasn’t good enough to meet Wall Street’s expectations, while poor guidance added to the gloom. But savvy investors can consider using the pullback as a buying opportunity since there are clear signs that the company is set to step on the gas in the future. The massive opportunity in the cloud infrastructure market could send Oracle’s stock soaring over the next five years.

Investors were quick to press the panic button following the company’s latest results as the 8% year-over-year increase in revenue and 4% jump in adjusted earnings weren’t enough to meet consensus estimates.

Moreover, management’s forecast of a 9% increase in revenue in the current quarter at the midpoint is slightly lower than the 11% that analysts were expecting.

But focusing on Oracle’s near-term performance and overlooking its long-term forecast is like missing the forest for the trees. The remarkable demand for the company’s cloud infrastructure for artificial intelligence (AI) training and inference is leading to phenomenal growth in its backlog.

This is evident from the 62% year-over-year increase in Oracle’s remaining performance obligations (RPO) last quarter to $130 billion. The metric refers to the total value of a company’s contracts that are yet to be fulfilled, and it is worth noting that this metric grew at a much faster pace than the company’s top line last quarter.

Oracle management pointed out on the latest conference call with analysts that the quarter was its strongest ever in terms of bookings. The company added $48 billion worth of new contracts to its backlog. At the same time, Oracle is constrained by capacity. The demand for the company’s cloud infrastructure is exceeding supply as more companies are turning toward Oracle’s offerings to train and deploy AI models and applications.

Management adds that its cloud infrastructure is “faster and, therefore, cheaper than our competitors.” The good part is that the demand for Oracle’s cloud infrastructure could keep growing at a terrific pace through the end of the decade. Goldman Sachs is estimating the cloud infrastructure-as-a-service (IaaS) market will generate $580 billion in annual revenue by 2030.

The pace of growth in Oracle’s RPO and the impressive rate at which it is signing new contracts suggest that the company is indeed on its way to cornering a lion’s share of the huge addressable opportunity. Importantly, the booming size of Oracle’s RPO is set to translate into stronger growth for the company in the coming years.

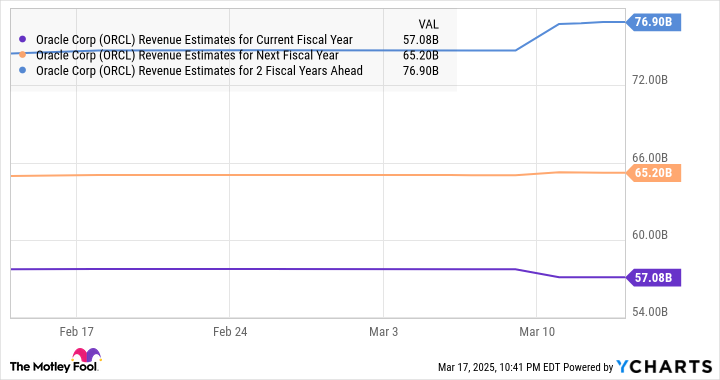

Oracle is expecting its revenue growth in the next fiscal year to accelerate to 15%, followed by a stronger jump of 20% in fiscal 2027. Both these numbers are higher than what the company was previously anticipating. Oracle had guided for $65 billion in fiscal 2026 revenue in September last year, but it now believes that it can hit $66 billion in revenue in the upcoming fiscal year.

Meanwhile, a 20% increase in its revenue in fiscal 2027 would send its top line to more than $79 billion. That’s higher than what analysts are expecting.

Investors would do well to note that Oracle could end up exceeding its own expectations in the long run considering the terrific pace at which it is increasing its data center capacity to meet demand. Management is going to double the capacity of its data centers in the current fiscal year, and it plans to triple the same by the end of the next fiscal year.

So, it is easy to see why Oracle is expecting an acceleration in its revenue growth, as higher data center capacity will enable it to fulfill more of its RPO. That, in turn, should ideally lead to strong growth in the company’s bottom line.

In September last year, Oracle projected that its earnings could increase at an annual rate of more than 20% through fiscal 2029. However, management’s comments on the latest earnings conference call suggest that it could do better.

Assuming Oracle can clock a 25% annual earnings growth rate over the next five years, its bottom line could jump to $18.31 per share by fiscal 2030 (using its projected fiscal 2025 earnings of $6.00 per share as the base). Oracle is currently trading at 21 times forward earnings, a discount to the tech-laden Nasdaq-100 index’s forward earnings multiple of 25.

If the market decides to put a higher valuation on Oracle and it trades at 25 times earnings in five years, that would put its stock price at $458. That would be a 197% jump from the stock price as I write this.

Investors should consider adding this AI stock to their portfolios following its recent drop. It is not just attractively valued right now; it has the potential to deliver healthy gains in the long run.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $305,226!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,382!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $517,876!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group and Oracle. The Motley Fool has a disclosure policy.